fools_gold wrote: ↑Sat Aug 22, 2020 12:00 amThe tax-free allowance seems to be the same regardless of the level of your contributions.Moneymatters wrote: ↑Fri Aug 21, 2020 6:24 am

Thanks!

So only years during which you contribute will build a tax-free allowance. That actually makes sense.

I'm guessing that even if you invest less than 40万 within a year you'll still get the 40万 allowance. (For each of the first 20 years.)

I think it is still preferential because your contributions aren't taxed. IDeCo allows you to defer the income tax on contributions to a later date.Moneymatters wrote: ↑Fri Aug 21, 2020 6:24 am Since 2017 you can continue to contribute when unemployed! Who knew..

https://dc.rakuten-sec.co.jp/resignation/#skip04-04

Depending on how much you contribute and what other income you might have when it's time to withdraw, this could still be preferential to just investing through a broker account and paying cap gains tax. But obviously limited choices of what to invest in.

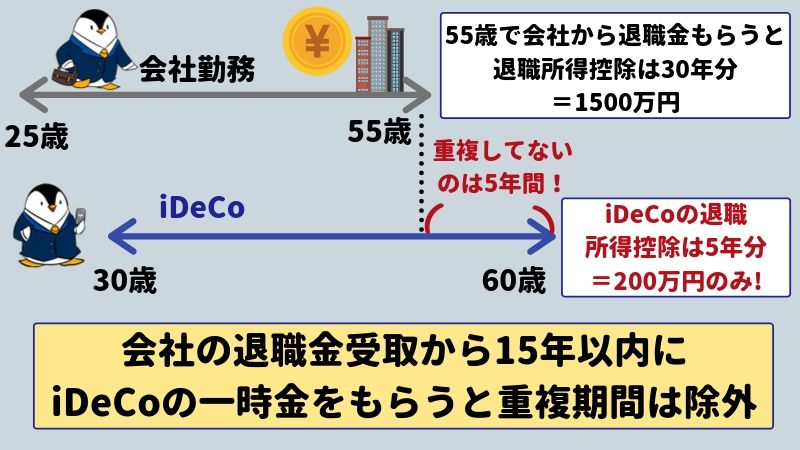

You can also receive it while you're working, but in that case I assume your basic allowance would already be used up so you could only get 60万円 tax free.Moneymatters wrote: ↑Fri Aug 21, 2020 6:24 am Another option for after 60 is to take ideco at 108万 per year tax free. (公的年金控除額60万円+基礎控除48万円).

This assumes no 退職 tax free allowance you can use and you don't have other pension income eating up that tax free allowance.

This has been very interesting! I hadn't thought really about the tax implications too deeply.

Certainly enlightening for me! Just to clarify this point.

I was saying that even if you are unemployed when making these contributions by investing cash on hand it might still be favorable.I think it is still preferential because your contributions aren't taxed. IDeCo allows you to defer the income tax on contributions to a later date.

At its most basic 400k per year would be tax free. But as you’d only be exposed to income tax on half of anything over the allowance and for many income tax on that amount could actually be less than 20.x of whatever capital gains you made.