I strongly suggest you check out https://shintaro-money.com/Juri wrote: ↑Mon Apr 19, 2021 10:43 am Hi there !

Sorry to bump this thread up but I had a question relative to Vanguard ETF and Vanguard in japan in general...

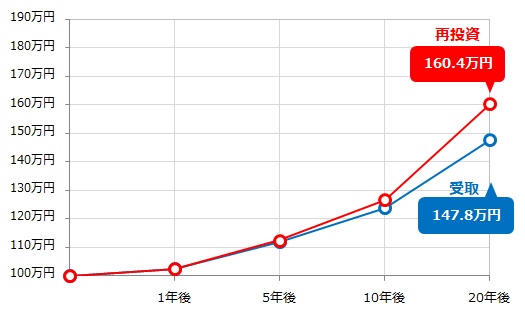

Even if the vanguard ETF VT and VOO have a small management fees, and with all the good we know about vanguard indexes, for a non US citizen is it still worth investing in those compare to the japanese non ETF equivalent (I'm thinking about the rakuten x vanguard total index or the eMaxis Slim ones for instance) ?

I still see a lot of europeans living here investing in those ETF funds but to me it feels a bit disadvantageous because of the double taxation (US + JP), the indivisible share (so the entry investment might be a bit steep and not customizable) and the absence of a DRiP (at least with rakuten).

What you think ?

Subsidiary question :

What would be a good non ETF equivalent of the vanguard BND ?

Thanks a lot if you can enlighten me on those points.

He goes in-depth on the differences and many popular index funds.

Cliffnotes

- Mutual funds are still a better deal than ETFs in Japan. (This is not the case in America, which is why MF have gotten a bad wrap recently).

- Emaxis Slim Funds are the best bet for most index funds.

- For 100% American funds the price difference is a wash, but Emaxis Slim funds are less trouble to purchase.

(None of this applies to Americans).

- If you prefer Vanguard products, Rakuten offers Wraps of a few of their funds, but with added cost basis.